A two-day rulemaking session started this Tuesday at the Department of Education. On the agenda is investigating whether the generous student loan repayment plan known as Pay As You Earn (PAYE) should be extended to borrowers who are currently ineligible. This session comes on the heels of a recent Politico report that raised concerns about the increasing cost of the student loan program.

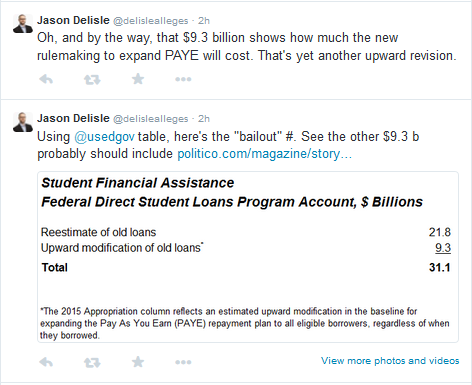

The report revealed a $21.8 billion budget shortfall in student loan revenue, sparking a range of reactions. Some argued that adjustments to profit estimates are to be expected and that, regardless of the shortfall, the program is still profitable. Others argued that $21.8 billion is a significant cost to the taxpayers that cannot be swept under the rug. Still others say that this adjustment is a one-time occurrence due to Obama’s recent policy changes regarding the terms of PAYE and loan forgiveness. If the DOE recommends further extensions to repayment plan eligibility, then this profit shortfall certainly won’t be one-time thing.

Of course, this debate re-opened the tired discussion of which accounting method should be used to determine the “real” cost of the PAYE program. Some, like Senator Deb. Fisher of Nebraska, argue that using the fair value accounting method would better reflect the cost of the program. This method makes the program look more expensive because it factors in the cost of the market risk. Others argue that the current accounting method is best since the lender is the government and the associated risks are different from those in the private market.

While these discussions are important, I think we are missing a crucial point. The loans that are been forgiven are essentially hidden and elusive grants: it is unclear who will most benefit from them. While increased funding for well-targeted Pell Grants is part of the government’s annual budget (which has to be approved and often fought over), these new repayment plans and forgiveness benefits are a matter of regulatory policy. This means that we are unaccountably doling out hidden grants. In some cases the forgiven loan can amount to much more than the maximum Pell. If we need to offer such great bailouts so that students do not default on their debts, then the government must be enabling the lending of bad loans.